Insuring a watch collection is one of the most important steps any serious collector can take. Whether the collection includes a single heirloom timepiece or dozens of luxury watches worth tens of thousands of dollars, standard homeowners insurance often falls far short of providing real protection. This guide walks through exactly how to insure a watch collection properly, from getting appraisals to filing a claim, with no fluff – just the steps that matter.

Key Takeaways

- Standard homeowners or renters insurance rarely covers the full value of a watch collection.

- A professional appraisal is the essential first step before buying any policy.

- Scheduled personal property coverage and specialty watch insurance offer the best protection.

- Documentation – photos, receipts, serial numbers – is critical for claims.

- Policies should be reviewed and updated regularly as collection values change.

- Premiums typically range from 1% to 2% of the total insured value per year.

Step-by-Step Guide to Insuring a Watch Collection

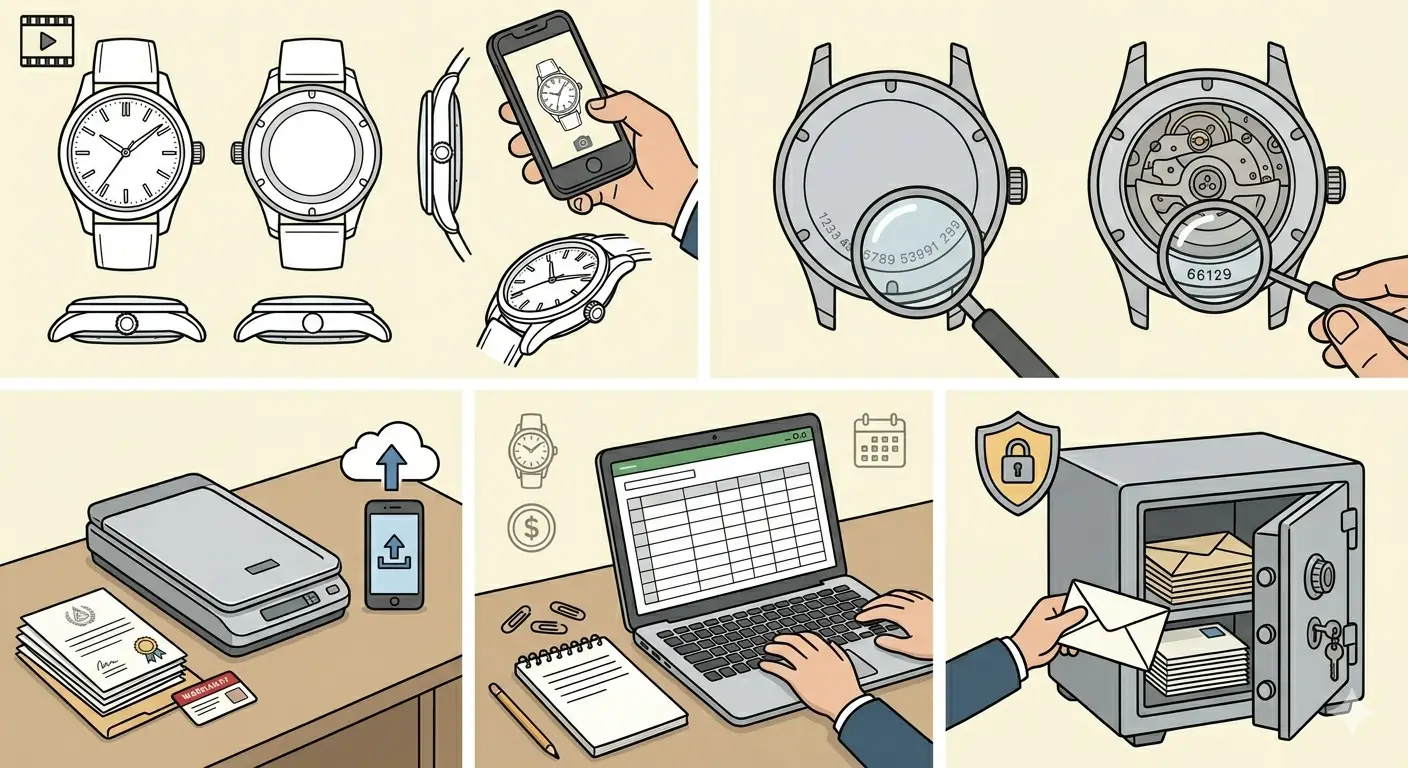

Step 1: Get a Professional Appraisal

Before contacting any insurer, every watch in the collection needs a certified appraisal. This is the foundation of the entire process. Without an accurate, documented value, it is nearly impossible to get proper coverage – or to receive a fair payout if something goes wrong.

- Step 1: Locate a certified watch appraiser through organizations like the American Society of Jewelry Appraisers (ASJA) or the National Association of Jewelry Appraisers (NAJA).

- Step 2: Bring all available documentation to the appraisal appointment – original receipts, warranty cards, service records, and the watches themselves.

- Step 3: Request a written appraisal report that includes the make, model, reference number, condition, and current replacement value of each watch.

- Step 4: Ask the appraiser about the difference between ‘replacement value’ and ‘fair market value.’ For insurance purposes, replacement value is almost always preferred.

Appraisals should be updated every two to three years, especially for watches from brands like Rolex, Patek Philippe, or Audemars Piguet, where secondary market values can shift significantly in a short time.

Step 2: Document the Entire Collection

Documentation is what turns an insurance claim from a stressful dispute into a smooth process. This step should happen before a policy is purchased, not after a loss occurs.

- Step 1: Photograph every watch from multiple angles – front, back, case side, and any unique markings or engravings.

- Step 2: Record the serial number of every watch. This is usually found on the case back or between the lugs at the 6 o’clock position.

- Step 3: Scan and store all receipts, appraisal certificates, warranty cards, and service records digitally using cloud storage.

- Step 4: Keep a written or spreadsheet inventory with each watch’s brand, model, reference number, year, purchase price, and appraised value.

- Step 5: Store physical copies of appraisals and receipts in a fireproof safe or a bank safe deposit box.

Keeping a well-organized record does more than just help with claims – it also makes the process of updating coverage much faster as the collection grows.

Step 3: Understand the Types of Watch Insurance Available

Not all insurance products are the same, and understanding the differences helps in choosing the right level of protection.

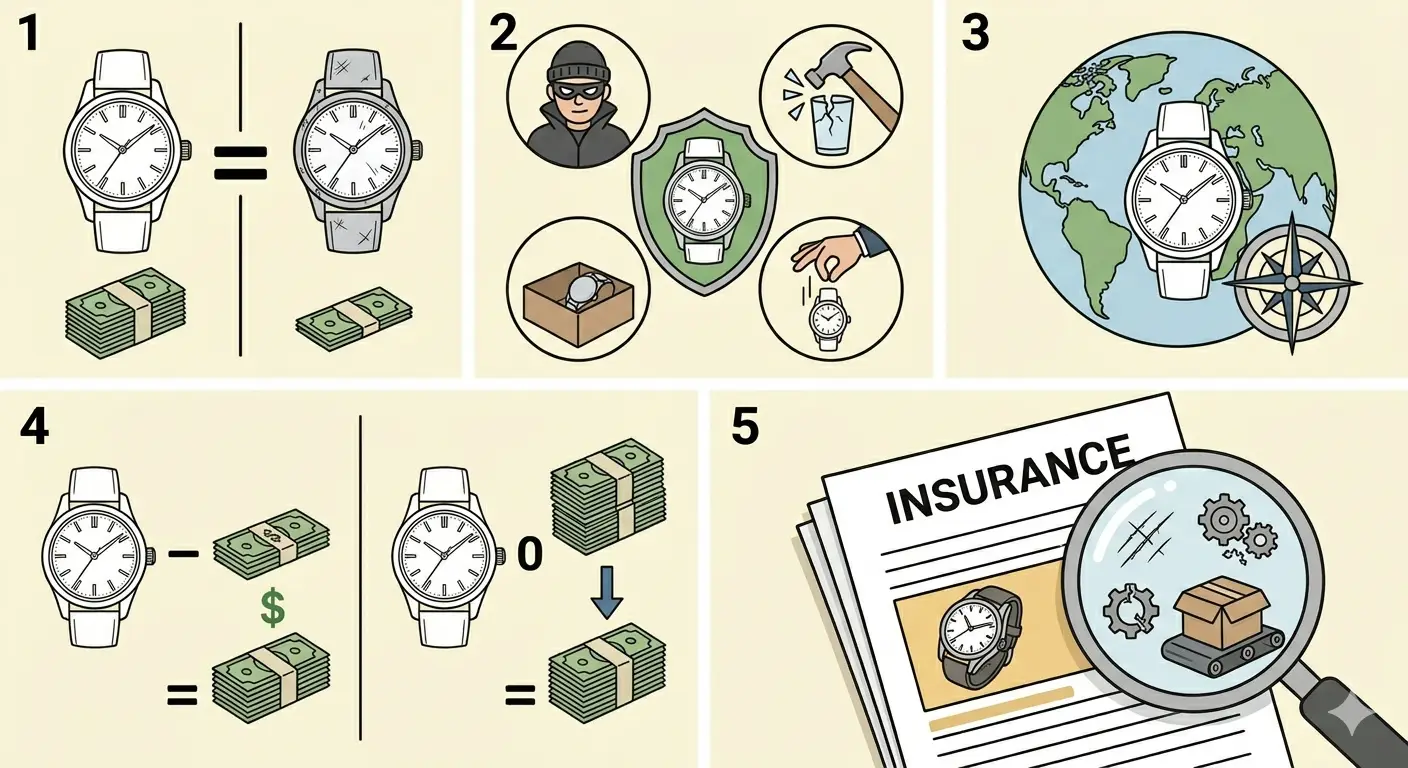

Homeowners or Renters Insurance: Most standard policies cover personal property, but watches are often subject to per-item sub-limits (commonly $1,000 to $2,500) and may exclude theft outside the home, accidental damage, or mysterious disappearance. For a serious collection, this alone is not enough.

Scheduled Personal Property (Floater or Rider): This is an add-on to a homeowners or renters policy that lists specific items individually. Each watch is covered for its appraised value, often with broader coverage than a standard policy. This is a solid option for smaller collections or collectors who already have a strong homeowners policy in place.

Specialty Watch and Jewelry Insurance: Companies like Jewelers Mutual, Chubb, and Hugh Wood Inc. specialize in insuring high-value collections. These standalone policies typically offer agreed value coverage, worldwide protection, coverage for mysterious disappearance, and no deductible options. For serious collectors, this is often the best route.

Step 4: Compare Policy Terms and Coverage Details

Once the type of coverage is clear, the next step is comparing actual policies. Not all policies that claim to cover watches offer the same protection. The key is to read carefully and ask direct questions.

- Step 1: Ask each insurer whether the policy uses ‘agreed value’ or ‘actual cash value.’ Agreed value means the insurer pays the full insured amount in a covered loss. Actual cash value accounts for depreciation, which can mean a significantly lower payout.

- Step 2: Confirm whether the policy covers all causes of loss – including theft, accidental damage, loss, and mysterious disappearance.

- Step 3: Check whether coverage applies worldwide. For collectors who travel or attend watch shows, this matters a great deal.

- Step 4: Ask about deductibles. Some specialty policies offer zero-deductible options, which can be worth the slightly higher premium.

- Step 5: Review any exclusions carefully. Common exclusions include wear and tear, mechanical failure, and loss during shipping without prior notification.

Pro Tip: Always ask for an ‘agreed value’ policy rather than an ‘actual cash value’ policy. If a Rolex Submariner is insured for $15,000 and stolen, an agreed value policy pays $15,000. An actual cash value policy may deduct for depreciation and pay significantly less – even if the watch has actually appreciated.

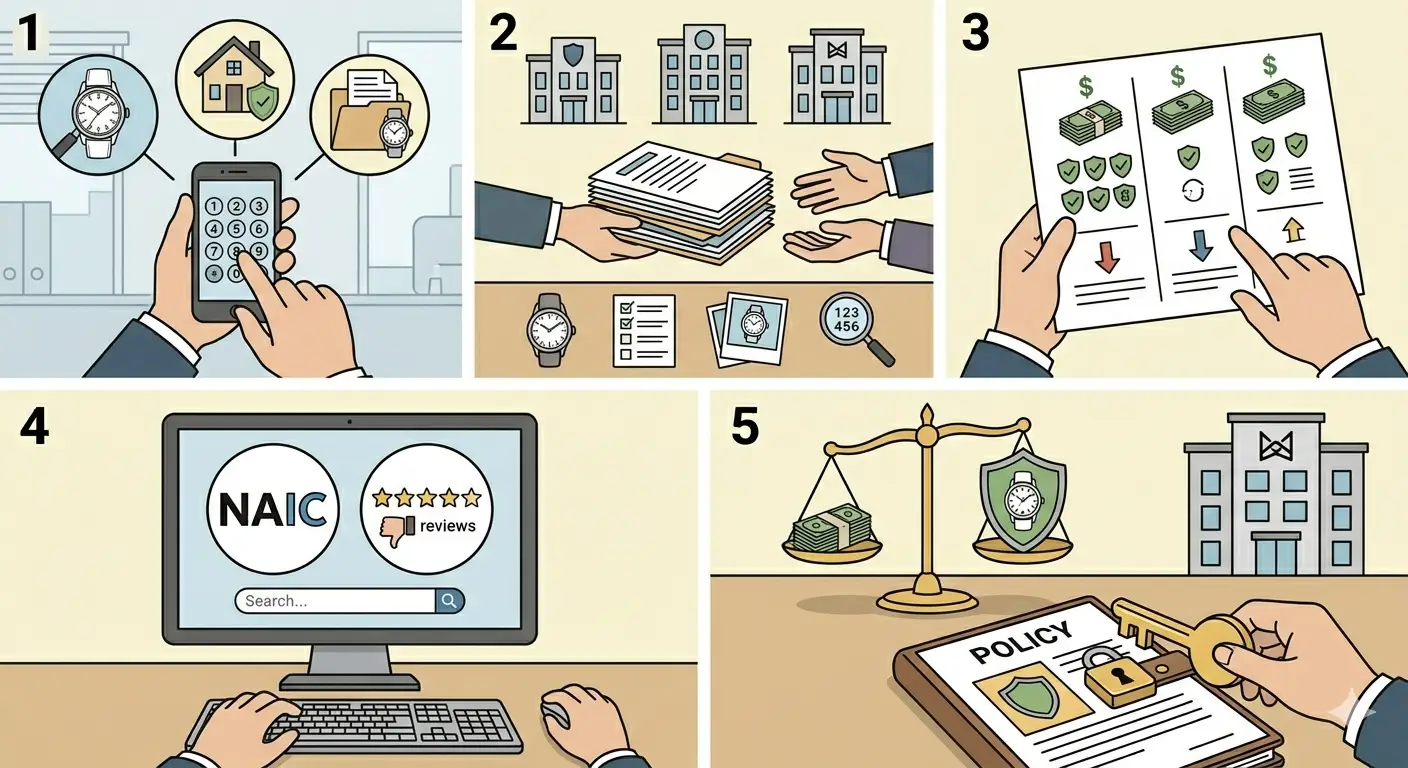

Step 5: Get Multiple Quotes and Choose a Policy

Getting at least three quotes from different providers is a smart move before committing. Premiums for watch insurance typically range from 1% to 2% of the total insured value annually. That means a $50,000 collection might cost between $500 and $1,000 per year to insure – a small price for genuine peace of mind.

- Step 1: Contact at least three insurers – a mix of specialty watch insurers and homeowners insurance providers offering scheduled property coverage.

- Step 2: Provide each insurer with the full documentation package: appraisals, inventory list, photos, and serial numbers.

- Step 3: Compare quotes not just by price, but by coverage scope, deductible, and claim reputation.

- Step 4: Check insurer reviews and complaint ratings through the National Association of Insurance Commissioners (NAIC) Consumer Information Source or AM Best.

- Step 5: Select the policy that best balances cost and comprehensive protection for the specific collection.

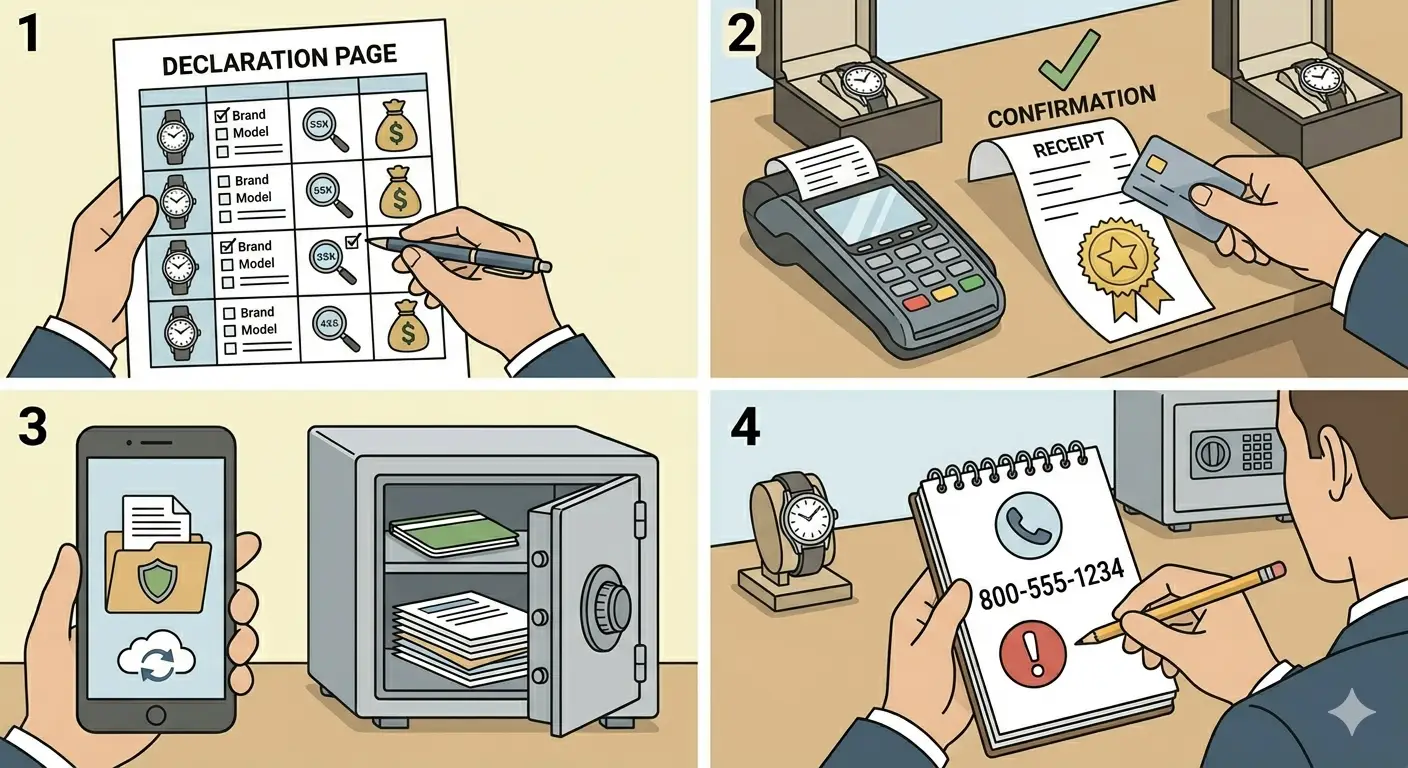

Step 6: Purchase the Policy and Store Proof of Insurance

Once a policy is selected, the final step before coverage goes live is completing the purchase and confirming all details are accurate.

- Step 1: Review the declarations page to confirm every watch listed is correct – brand, model, reference number, and insured value.

- Step 2: Pay the premium and receive confirmation of coverage in writing.

- Step 3: Store the policy documents digitally and keep a physical copy in a safe location separate from the watch collection.

- Step 4: Note the claims contact number and process in case it is needed quickly after a loss.

Step 7: Review and Update Coverage Regularly

A watch insurance policy is not something to buy once and forget. Collections grow, values change, and what was adequate coverage two years ago may leave gaps today.

- Step 1: Review the policy annually – ideally at renewal time.

- Step 2: Add any new acquisitions to the policy immediately after purchase. Coverage usually needs to be added within a short window (often 30 to 90 days) for new items to be protected.

- Step 3: Update appraisals every two to three years or after significant market changes.

- Step 4: Remove watches that have been sold or gifted from the policy to avoid paying unnecessary premiums.

Pro Tip: Set a recurring calendar reminder – perhaps using a clock tab or scheduling tool – to review the watch policy each year. Markets move fast, and a Rolex or AP bought two years ago may now be worth 30% to 50% more. Underinsurance is one of the most common and costly mistakes collectors make.

Storage and Security Tips That Can Lower Premiums

Insurers often reward collectors who take active steps to protect their watches. The right storage and security setup can reduce premiums and strengthen any claim if a loss does occur.

- Store watches in a quality watch safe or vault that is bolted to the floor or wall. Many insurers require safes for high-value items.

- Install a monitored home security system. Some insurers offer discounts of 5% to 15% for professionally monitored alarm systems.

- Avoid posting collection photos publicly on social media – this is a known way thieves identify high-value targets.

- When traveling, use a discreet, hard-sided travel case and keep watches in carry-on luggage, never in checked bags.

- Consider a bank safe deposit box for watches that are rarely worn. Some insurers offer reduced premiums for items stored in bank vaults.

Common Problems and Troubleshooting

Problem 1: Claim Is Denied Due to Missing Documentation

This is the most common issue collectors face after a loss. If serial numbers, appraisals, or proof of purchase cannot be provided, insurers may reduce or deny the claim. The fix is prevention – build and maintain a digital documentation file before anything goes wrong. If documentation is currently incomplete, start now by photographing every watch and recording serial numbers. Then schedule professional appraisals for any watch without a current certificate.

Problem 2: Insured Value Is Too Low After Market Appreciation

Watch values – particularly for Rolex, Patek Philippe, and vintage pieces – can increase dramatically. A watch insured for $8,000 three years ago may now sell for $15,000 or more. If a claim is filed, the payout will be based on the insured value, not the current market value. The solution is to update appraisals regularly and adjust coverage whenever significant appreciation occurs.

Problem 3: Standard Homeowners Policy Does Not Cover Theft Outside the Home

Many collectors discover this limitation only after a watch is stolen while traveling or at a watch event. Standard homeowners policies often limit off-premises coverage or exclude it entirely for high-value items. Switching to a scheduled property rider or a specialty watch policy with worldwide coverage solves this gap.

Problem 4: Insurer Requires a Safe or Vault for Coverage to Apply

Some policies include conditions that watches must be stored in an approved safe when not being worn. If a watch is stolen while stored improperly – say, left in an unlocked drawer – the insurer may deny the claim. Read policy conditions carefully and invest in appropriate storage before the policy is purchased.

Tips for Watch Collectors Buying Insurance

- Use a specialist broker who works with watch and jewelry insurance regularly. They know which insurers offer the best terms for specific types of collections.

- For a large or growing collection, consider working with an estate attorney alongside an insurance advisor to ensure the collection is also protected from a legal and inheritance standpoint.

- Keep track of purchase dates and service records. When making a claim, this timeline helps establish ownership and authenticity.

- If the collection includes vintage or limited-edition pieces, look for insurers who specialize in these categories. Valuing a vintage Heuer Carrera is very different from valuing a current-production watch, and a generalist insurer may undervalue it.

- When timing matters – such as notifying an insurer about a new acquisition within a specific window – use a reliable world time comparison tool to ensure deadlines are met correctly across time zones, especially when dealing with international insurers.

Frequently Asked Questions

Does homeowners insurance cover a watch collection?

Standard homeowners insurance does cover personal property, but it almost always includes sub-limits for watches and jewelry – often $1,000 to $2,500 per item. For most serious collections, this is far below the actual value. A scheduled property rider or specialty watch insurance policy is needed for proper coverage.

How much does it cost to insure a watch collection?

Premiums for watch insurance typically range from 1% to 2% of the total insured value per year. A collection appraised at $30,000 would generally cost $300 to $600 annually to insure. Factors like storage security, location, and claims history can affect the final rate.

Do watches need to be appraised before getting insurance?

Yes. A professional appraisal is required by most specialty insurers and is strongly recommended even for scheduled property riders. Without an appraisal, the insured value may be set too low, leaving the collector underinsured in the event of a claim.

What is the difference between agreed value and actual cash value for watch insurance?

Agreed value means the insurer pays the full amount listed in the policy if a covered loss occurs, with no depreciation applied. Actual cash value factors in depreciation and can result in a significantly lower payout. For watches – which often appreciate in value – agreed value coverage is strongly preferred.

Does watch insurance cover accidental damage?

It depends on the policy. Standard homeowners policies generally do not cover accidental damage. Specialty watch insurance policies and many scheduled property riders do cover accidental damage, including cracked crystals, water damage beyond the watch’s rated depth resistance, and drops. Always confirm this with the insurer before purchasing.

Is a watch covered if it is stolen while traveling?

Not always. Standard homeowners policies often limit or exclude off-premises theft. Specialty watch insurance policies and scheduled property riders that include worldwide coverage will cover theft while traveling. Always verify that the policy specifically includes coverage outside the home.

How often should watch appraisals be updated?

Appraisals should be updated every two to three years as a baseline. For watches from brands with rapidly changing secondary market values – like Rolex, Audemars Piguet, or Patek Philippe – annual updates may be more appropriate. An outdated appraisal can result in a payout that is thousands of dollars below the current replacement cost.

Can a watch be insured if the original receipt has been lost?

Yes. A current professional appraisal from a certified appraiser can substitute for the original receipt in most cases. Photographs, serial numbers, service records, and any other documentation that establishes ownership and value will strengthen the application.

What should be done immediately after a watch is lost or stolen?

Report the loss to local police and obtain a police report number. Contact the insurance provider as soon as possible – most policies have a notification requirement, often within 24 to 72 hours of discovery. Provide the insurer with all available documentation: serial number, photos, appraisal, and the police report. Avoid making any statements that speculate about how the watch was lost until all facts are clear.

Are vintage or rare watches harder to insure?

They can require more documentation and a specialist appraiser, but they are absolutely insurable. Specialty insurers who focus on watches and fine jewelry are best equipped to handle vintage, limited-edition, or high-complication pieces. Using a standard insurer unfamiliar with the vintage watch market can result in significant undervaluation.